In describing patterns of construction and building permits in recent decades, they write: "During the subprime boom, construction of single-family homes surged to a high of 1.8 million units per year, far above the 1.1 million units required to cover population growth and physical depreciation of structures. Construction then collapsed, falling roughly 75 percent from the peak by mid-2009." As their figure shows, this decline appears to have bottomed out at a level fairly similar to that experienced in the deep recessions of the early 1980s.

They emphasize the role of swings in the loan-to-value ratio: "More people qualified for a mortgage during the so-called subprime boom because lenders eased the minimum down-payment ratios, maximum debt-payment-to-income ratios, minimum credit scores and other criteria. The relaxed credit standards can be seen in a new survey-based data series on the average mortgage-loanto-

house-price ratio, or loan-to-value (LTV) ratio, for first-time homebuyers (Chart 3), or its counterpart, the downpayment ratio. The average, cyclically adjusted LTV ratio rose to as high as

94 percent (that is, a 6 percent down payment) at the height of the subprime boom, before retreating during the bust. The ratio was about 88 percent (12 percent down payment) during the 1990s."

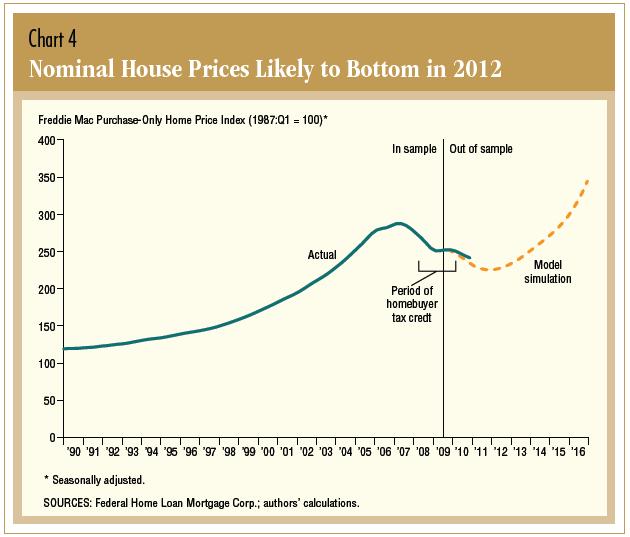

Their simulation results suggest that housing prices will bottom out in late 2011 or 2012. "During the boom and subsequent bust, house prices were affected by unusual factors, including large swings

in mortgage financing standards and tax credits for first-time homebuyers. ... Our econometric models of U.S. house prices, estimated using data through third quarter 2009, take account of these factors, as well as conventional drivers of housing demand. This exercise, carried out in early 2010, predicted

that house prices would resume declining after the expiration of the U.S. tax credit in mid-2010, falling about 5 to 6 percent after third quarter 2010 before likely hitting bottom in late 2011 or early 2012 (Chart 4). ... Since early 2010, our simulation has tracked the actual movement in the Freddie Mac purchase-only home price index."

0 comments:

Post a Comment